Many contractors remain bullish on multifamily housing demand; this risks an oversupply problem--especially for luxury and high-end developers at a particularly dangerous time.

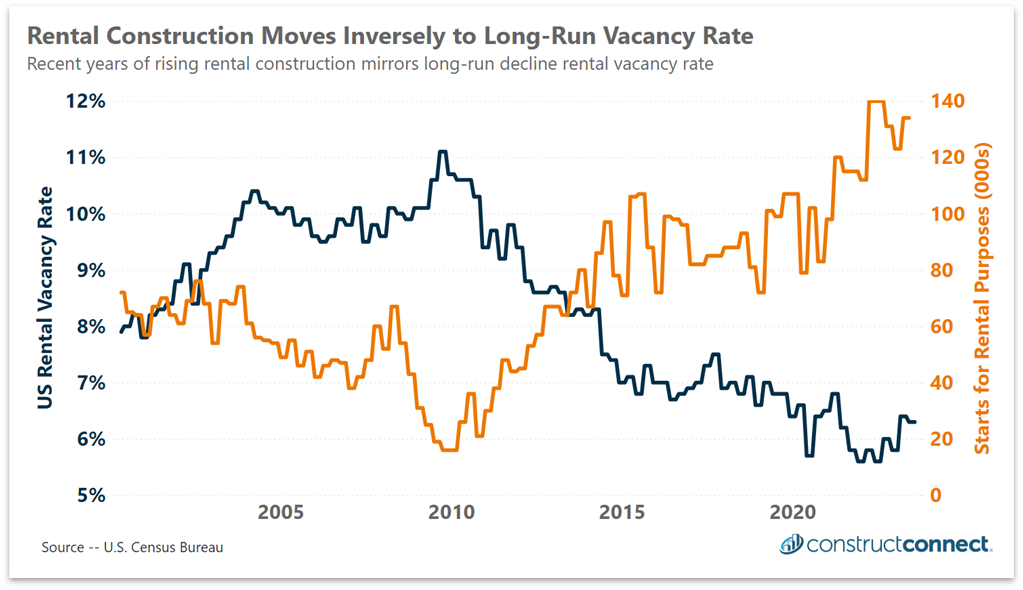

Several firms have come to our economics team in recent weeks to request guidance on the high-end of this market. Some of these inquirers may not realize that they are late to this market play based on existing multifamily starts data. Furthermore, in traditional industries such as construction, where investment outlays must be made months and years in advance of the finished structure, it can be easy for supply and demand to change, and with such changes, revenue and profit expectations. In today’s multifamily market, it appears that years of falling vacancy rates and sharply rising rental prices have provoked today’s run-up in new multifamily starts.

The aftermath of the Great Recession experienced a long-run decline in rental vacancy rates. This decline prompted a rebound in the number of multifamily starts built for rental purposes to a sustained seasonally adjusted level of around 80,000 to 90,000 units per quarter between 2015 and the end of 2019. In the immediate quarters following COVID, vacancy rates fell a full percentage point, returning to lows last witnessed in the early 1980’s. This, combined with other COVID market shocks, helped to trigger a 60% increase in multifamily rental starts. As recently as the third quarter of 2022, multifamily rental starts topped 140,000 units quarterly.

Such changes beg the question: if every contractor is making the same play and adding supply during a time of turbulent housing dynamics, how will supply and demand equalize when it comes time to fill all these new structures with tenants? Will every developer profit from their investment? Will there be enough renters to achieve the occupancy rates necessary to achieve the expected ROI for these projects? Further, with anecdotal evidence suggesting that many developers desire to supply the smaller premium end of this market, what would happen to the market in total from an oversupply of top-end units? Would falling luxury rental prices impact the mid-priced market?

Additionally, the dynamics of the rental market will be impacted by changes and shocks to the single-family market. Today’s single-family homes are historically unaffordable due to a combination of high prices and high interest rates, and this corroborates with the National Association of Realtor’s Housing Affordability Index Housing, which since June 2023 has been at an all-time low.

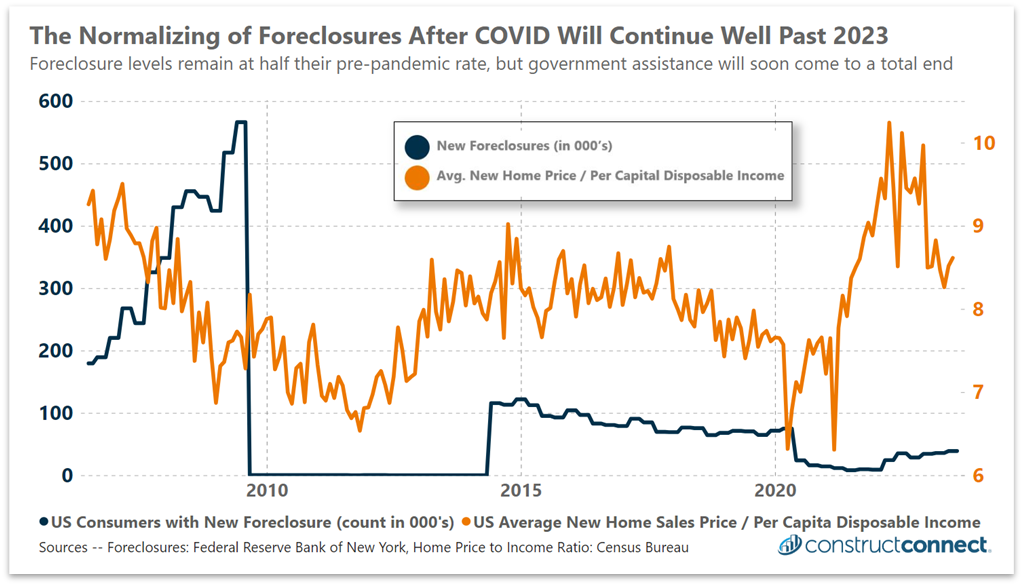

Bringing further complexity to the problem is the hesitancy of existing homeowners to surrender their 3% mortgages by selling their property. Supply remains further restricted by the government’s COVID mortgage forbearance programs. The lingering effects of such programs will continue to suppress the natural level of foreclosures until at least November 2023, according to HUD. In short, the entire housing market in the coming years will be significantly impacted by a slew of powerful market forces, many of which will shift supplies along with altering prices.

Expectations at the Federal Reserve are for the Fed Funds Rate, and by extension mortgage rates, to begin falling in 2024 and continue moving lower through 2025. Assuming these expectations hold true, the housing market could see a significant recovery in the volume of existing single-family homes on the market in two years or less, potentially sending luxury unit renters back to the single-family market as either buyers or renters. As supply and demand conditions change at the top of the rental market, its effects could depress prices at the mid and lower tiers of the rental market.

Historically, the amplitude of previous market booms and busts has correlated with the number of market participants all making the same bet. The more participants that take the same action, the more severe any future market correction will likely be. In the construction industry, this may mean that the most desirable geographies, which are today attracting multiple developers, may experience greater supply hangovers in the future and the greatest profitability pressures. In contrast, those “second tier” geographies that have and continue to draw less attention from many developers may become the better bets.