Rebuild of Baltimore’s Key Bridge to Start

The Maryland Transportation Authority (MDTA) project to rebuild the Key Bridge is scheduled to start this week, authorities said (weather permitting)

Can public spending continue to play the role of industry backstop while public finances steadily become untenable?

The benefits to a business of revenue diversification are well chronicled in the construction and manufacturing space. Anecdotal evidence during the Great Recession revealed that diversified firms serving two or more verticals often found themselves in far better shape during and after the recession than their non-diversified peers. For undiversified firms, a slowdown in the single vertical they serviced —or for some, even a single large customer— presented an existential threat to their survival. These firms often had no choice but to lay off experienced staff just to keep themselves solvent. However, as the economy rebounded these firms were unable to take on work for lack of key employees. Unable to convert the economic rebound into new business such firms never truly recovered, falling distantly behind their competition. In contrast, more diversified firms were better able to retain their best employees and during the rebound hired the best of those who had been laid off. Lost access to skilled workers in many anecdotal cases was the single greatest reason why non-diversified firms failed to recover even if they survived the worst of the recession.

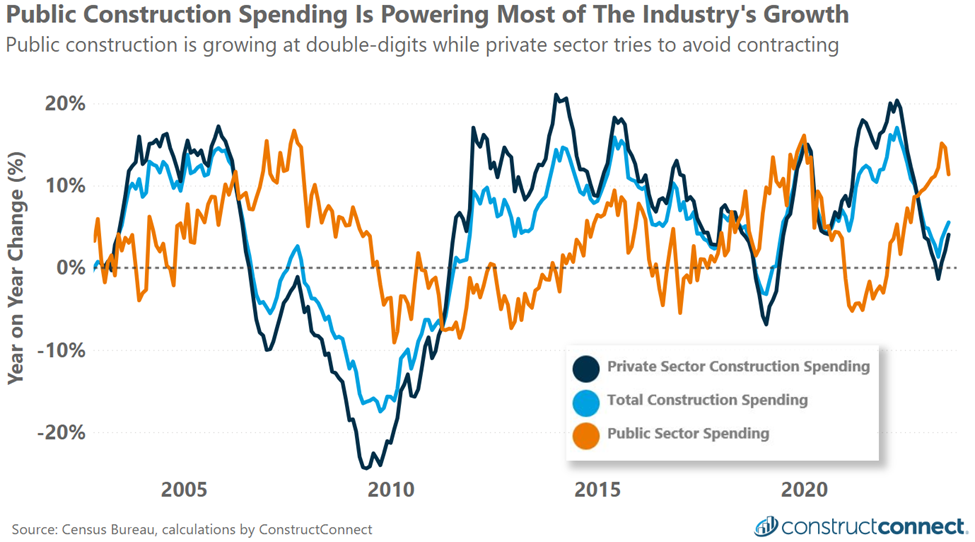

Such stories may seem anachronistic given the growth of both private and public construction spending in the recent past. However, incipient matters today will pose significant threats to both future private and public construction demand, making past lessons on diversification germane once again. Looking beyond the fanfare around electric-vehicle plants, battery plants, and other multi-billion dollar “mega” projects private-sector construction spending growth has decelerated since early 2022. Adjusting for construction price inflation, 2023 private construction spending through August has been either flat or contracting from year-ago levels. One cause for this is rising interest rates which by increasing financing costs has lowered investment returns.

Conversely public construction spending has quickly accelerated since 2022 thanks to the passage of major federal infrastructure bills, allowing for new spending on public construction to supplant slowing private sector spending. In the periods immediately following each of the three recessions prior to 2020, rising public construction spending provided private construction time to recover from a recession. In this way public construction spending has historically served as a backstop and safety net for industry revenues.

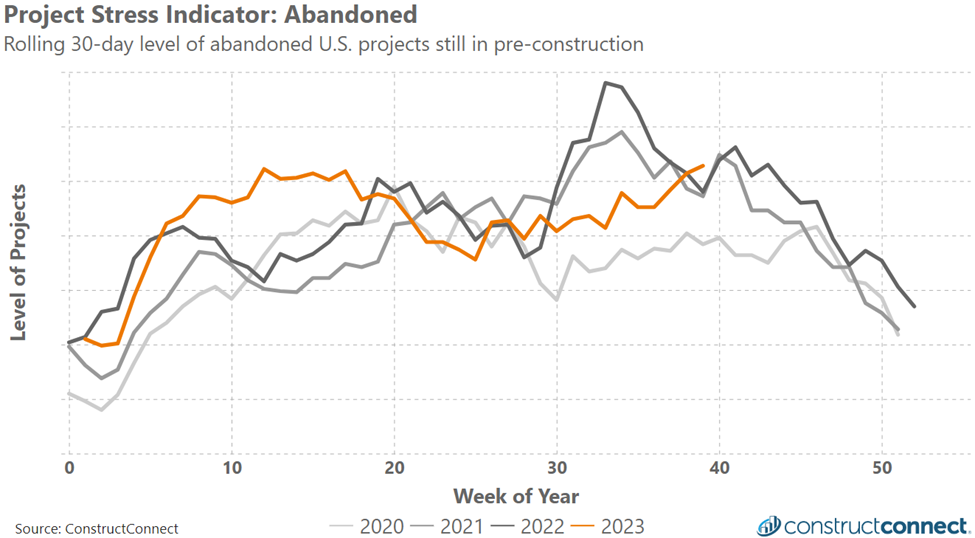

As we have moved further into this year, warning indicators of future private sector growth have continued to flash with concern. ConstructConnect’s Project Stress Index observed a surge in abandoned projects at the start of the year and more recently once again in the third quarter. Both surges in abandoned project levels were almost exclusively the result of rapid changes in private sector data.

In contrast public projects, which are not subject to the same funding restraints as private-sector projects, have reported year-to-date stress levels that follow historic norms. Recent years of legislation have in fact generated a surge in public and publicly subsidized construction which has led to a boom in mega-projects across the country. Recent research suggests that mega projects presently account for about 1/3rd of total nonresidential construction.

Unfortunately, the sector’s dependence on public construction spending to carry it through future recessions will face a rising number of challenges in just the next few years. The federal government’s inability to adhere to a balanced budget for most of the last 50-years has made the government functionally dependent on debt. In 2022, 80% of discretionary spending, which includes but is not limited to spending on public construction, education, military, and interest on the national debt was made possible only through regularly taking on yet more debt. Moving forward, rising interest rates, heightened geopolitical tensions, and rising nondiscretionary expenses —especially for Medicare and Medicaid costs— will make the nation’s debt dependence untenable without either vastly increasing taxation, or through extremely painful spending cuts to discretionary spending.

Public construction’s unspoken dependence on debt markets and the Federal government’s diminishing ability to continue operating as it has in the past jeopardizes the ability of public projects to serve as an industry backstop in future recessions. Without this backstop the industry should expect more severe business cycle contractions during future recession. For those industry leaders accustomed to shrewdly diversifying their revenue streams through a combination of both public and private work, tomorrow’s best strategy may involve a reduced dependence on public work and a greater reliance on a multitude of private sector verticals.

The Maryland Transportation Authority (MDTA) project to rebuild the Key Bridge is scheduled to start this week, authorities said (weather permitting)

Construction is underway on the long-awaited King Empowerment Center, the first new school project for Kansas City Public Schools (KCPS) in more than...

Senior Economist Michael Guckes discusses whether the past behavior of new and unfilled orders is an ominous sign of things to come for the...

Despite the recent improvement of supply chain performance, specific supply chain problems continue to frustrate specific areas and regions.