September Expansion Pace Quickens on Gains in Medical, Government, & Community

ConstructConnect’s Expansion Index for September 2022 was 10% and 20% higher overall in Canada and the United States, respectively.

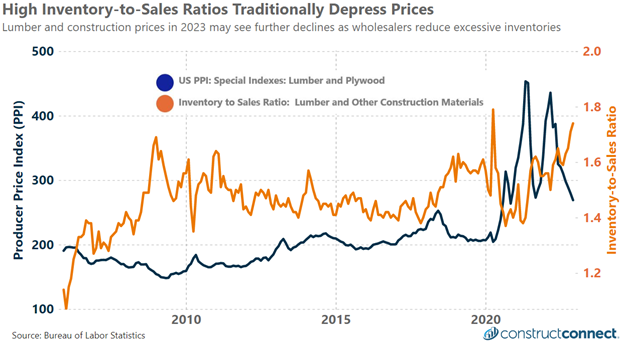

Inventory-to-sales levels can be helpful indicators of where the balance between supply and demand stands for various categories of products. If and when wholesaler and manufacturer inventory levels become bloated, it can lead to lower prices downstream for end-users, including trades and general contractors, as upstream suppliers reduce prices to protect their market share from competitors.

The latest inventory-to-sales ratio (I/S ratio) data for lumber and construction materials, released in early February by the U.S. Census Bureau and representing December 2022 activity, issued a reading of 1.74. This result, the second highest in history, exceeds all readings during the building boom and bust of the Great Recession and is only exceeded by a one-month anomaly reading taken in April of 2020 resulting from COVID-19 shutdowns.

Since COVID-19, there have been several whipsaw movements in the I/S ratio data, the first of which occurred early in the pandemic when government regulations shut down lumber mills. Once mills were allowed to reopen, they were unable to catch up with demand. As a result, I/S ratios fell to a decade low, and lumber prices more than doubled by mid-2021, according to the Bureau of Labor Statistics.

The Bureau’s index, however, fails to capture the unprecedented gyrations that were happening behind the scenes. Lumber contracts on commodity exchanges moved much more drastically, with lumber futures rocketing from under $200 pre-pandemic to more than $1,600 in early 2021. As of late February, a March 2023 random-length lumber futures contract was trading at $383, a far cry from the $1,400 price similar contracts commanded just one year ago.

The rapid rise in the construction I/S ratio during 2000 and again in 2006-2007 preceded a broader economic recession by 6-12 months. The latest rise from a decade-low reading of 1.38 in early 2021 to a historically high reading at year-end 2022 bodes very poorly for the future of the economy if history should repeat itself. Secondly, the recent and thus far unabated ascent of the I/S ratio clearly signals that the supply and demand dynamics of the construction materials markets have changed significantly in the last year.

Until these dynamics change, material prices seem destined to remain depressed, allowing those contractors with lean inventories to buy goods as needed at some of the lowest prices in more than a year. In contrast, those who have kept high inventory levels over the last year not only paid more for such goods in general but must continue to pay the carrying costs for that inventory.

ConstructConnect’s Expansion Index for September 2022 was 10% and 20% higher overall in Canada and the United States, respectively.

January 2023 lumber futures, as of January 4, 2023, were quoted at $475, a decline of more than 26% from a late October high of $643.50.

ConstructConnect’s Expansion Index for December 2022 was 5% and 21% higher overall in Canada and the United States, respectively.

The Louisiana Legislature opened its 2025 regular session in April by approving a sweeping list of over $1 billion in highway construction projects