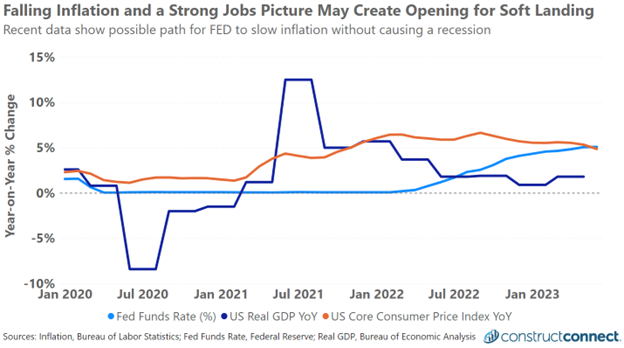

On July 26, the Federal Reserve increased the benchmark Fed Funds Rate (FFR) to 5.25%, marking the 11th consecutive time that the Fed has raised rates since early 2022. Never in history has the Fed raised the FFR this aggressively. As the Fed increases the FFR, it indirectly raises the cost of borrowing for public and private borrowers. This benchmark, which influences the rate of all other U.S. debt products, is presently at its highest level in more than 22 years.

The FFR is arguably one of the more important tools the Fed has for regulating inflation; however, adjustments to the FFR have consequences for the economy that extend well beyond simply influencing inflation. Chiefly, as the FFR increases, it also raises the cost of borrowing capital. As the cost of borrowing increases, it reduces the number of borrowers willing to take out debt at higher rates, thereby slowing investment spending and overall economic growth.

For this reason, the Fed has a challenging goal of raising the FFR enough to slow inflation while keeping it low enough to avoid a recession. Finding the right balance between these two goals is no easy task, as adjustments to the FFR can result in unintended consequences to the economy.

At the start of 2023, polls of economists overwhelmingly indicated little hope of the Fed being able to successfully combat inflation without also sparking a recession. However, seven months on and with inflation slowing and GDP growth remaining positive, the Fed has exceeded the expectations of many despite there still being much work left for the Fed to do to achieve its self-imposed goal of lowering inflation to around 2%.

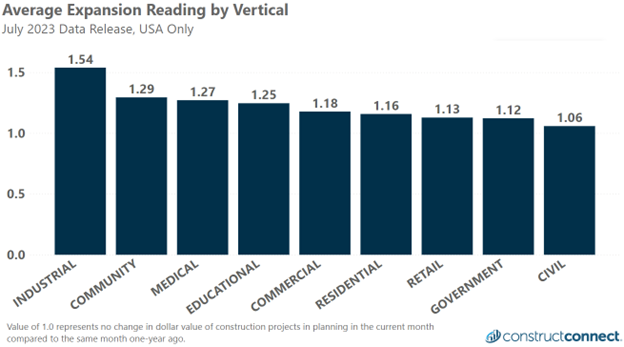

For the construction industry, a rising FFR is synonymous with rising borrowing costs for owners and developers of forthcoming construction projects. Despite rising borrowing costs, several verticals within the construction space continue to report strong contemplated spending growth from year-ago levels. Contemplated industrial spending as of June reported a 54% increase from year-ago levels.

Copacetic with this outlook is ConstructConnect’s Starts forecasts beginning in 2024 and extending through 2027. All three of the company’s category level (civil, nonresidential, and residential) forecasts during these years expect mid-single-digit spending growth. A welcomed change from the contractionary results forecasted for full year 2023 in both the nonresidential and residential categories.

However, not all is well, as U.S. banks reported a collective $9.2B in Commercial and Industrial loans more than 90 days past due during the 6-month period ending March 31, 2023. This recent spike in distressed debt is eerily similar to the debt spike which occurred during the Great Recession.

Another sign of economic distress has manifested itself in the form of high short-term yields and relatively lower long-term yields, known as a yield curve inversion. Such a condition typically occurs because of expectations that the central bank will have to cut future rates in hopes of correcting the economy out of a recession. Over the last 50 years, rate inversions have accumulated an unbeatable record in foreshadowing recessions in America.

Looking forward, the Fed has signaled to Wall Street that it intends one more rate increases this year, potentially raising the FFR to 5.75% before year’s end. Should this year’s adjustments to the FFR put inflation on a trajectory that sets inflation on a downward trend toward 2%, then expectations will be for the Fed to begin lowering the FFR, and borrowing costs overall, sometime beginning in 2024.

According to the Federal Reserve’s own predictions for 2024 and 2025, they expect median FFR rates of 4.6% and 3.4%, respectively. This falling trajectory of the FFR will help to reinflate the economy and, in particular, capital-intensive investments and projects a certain tailwind for the construction industry.