Expansion Index Points to Regional Shift, Optimism vs Starts

Nonresidential construction starts lackluster year-to-date from a year ago. However, the ConstructConnect Expansion Index paints a more optimistic...

Much has been made of the efforts by the U.S. Federal Reserve Bank to raise interest rates in order to cool down price inflation without also sending the overall economy into a recession. Achieving this feat will be a considerable task as it requires the right balance of slowing down the various elements of total economic activity, as measured by Gross Domestic Product without sending it into reverse.

Of the four traditionally recognized components (consumption, investment, government, and net exports), investment spending is arguably one of the more rate-sensitive components of GDP due to the large amount of debt financing which underpins much investment spending. As interest rates increase, the cost of borrowing money used for making investment purchases increases, driving up the cost of such projects and driving down their return.

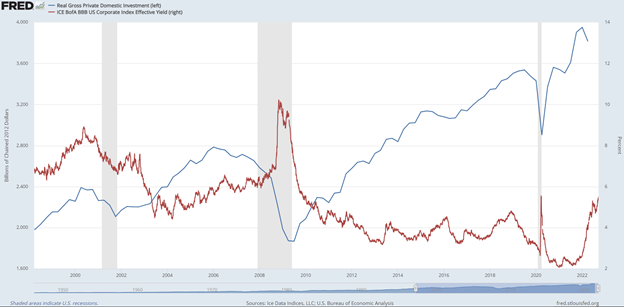

The Federal Reserve’s transition from a decade of easy monetary policy starting after the Great Recession toward tighter policy in recent months is evident by the net flows of bond debt held by corporations outside the financial sector. Corporate bond growth which has historically grown by 5% on average since at least the late 1990s was recorded at 0.5%, or one-tenth of historical growth levels according to Q2 2022 data provided by the Bureau of Economic Analysis.

At the more aggregate level of total U.S. investment spending, the impact of the ascent of corporate bond rates since mid-2021 was felt in the latest quarter’s investment data in which inflation-adjusted investment spending contracted by $137 billion or 3% from the prior quarter’s record high. While a single quarter of contracting investment spending is not indicative of a recession, history does have many instances in which multiple quarters of falling investment spending precede a recession as evident in the dot-com recession of 2000 and the Great Recession of 2008.

To the degree that construction spending is dependent on financed (borrowed) capital, the implication for the construction spending industry is clear: rising financing costs will erode demand for new construction investment, and in particular for those projects which are expected to have lower returns on investment. For this reason, the impact to the overall construction industry will not be uniform; rising rates will have a lesser impact on infrastructure spending for highly demanded goods which in 2022 will include computer chip foundries, electric vehicle manufacturing, and associated battery assembly and specialty metals mining.

Conversely, industries with lower rates of return—historically this has included retail and services—will feel the pain of rising borrowing costs more acutely. As rising rates send already modest ROIs below acceptable levels, or even negative, investment spending will quickly recede and project cancellations rise. Construction firms that specifically serve these worst affected markets will have the hardest time moving through this rising-rate environment.

There are many actions that the construction industry can take to avoid the worse of a rising-rate environment:

Nonresidential construction starts lackluster year-to-date from a year ago. However, the ConstructConnect Expansion Index paints a more optimistic...

The seasonally adjusted unemployment rate has been less than 4.0% for 15 months in a row, indicative of a labor market that’s about as tight ever.

In mid-2022, overall inflation by some measures was approaching 9%, a 40-year high following more than a decade of historically low inflation rates.

See how the ongoing financial health of chipmakers could impact construction investment on semiconductor chipmaking plants.